Introduction to the CSDDD

Kristy Duane

In this video, Kristy Duane from CMS provides an overview of the Corporate Sustainability Due Diligence Directive (CSDDD), a key component of the European Green Deal aimed at fostering sustainable and responsible corporate behaviour.

In this video, Kristy Duane from CMS provides an overview of the Corporate Sustainability Due Diligence Directive (CSDDD), a key component of the European Green Deal aimed at fostering sustainable and responsible corporate behaviour.

Introduction to the CSDDD

13 mins 3 secs

Key learning objectives:

Understand what the current status of the Corporate Sustainability Due Diligence Directive (CSDDD) is

Identify who the CSDDD applies to

Understand when the CSDDD comes into effect

Overview:

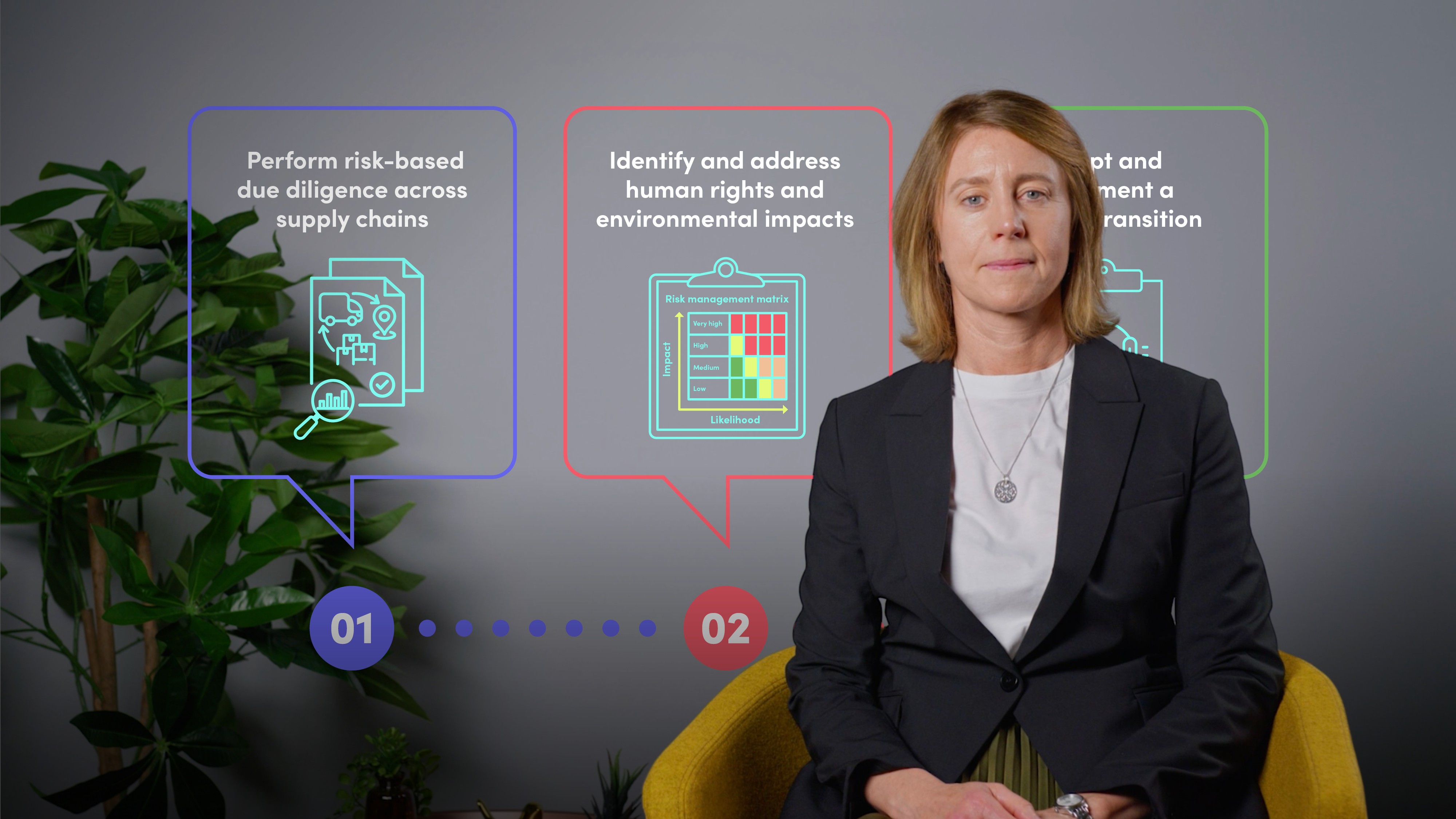

The CSDDD mandates that certain companies conduct risk-based due diligence across their supply chains to identify and address adverse human rights and environmental impacts. In addition they require these companies to adopt and implement a climate transition plan. This directive represents a shift from soft law to legally enforceable obligations.

Summary

What is the Corporate Sustainability Due Diligence Directive (CSDDD)?

The CSDDD is a directive that forms part of the European Green Deal, aimed at making the EU climate-neutral by 2050. It requires in-scope companies to perform risk-based due diligence on their supply chains to identify and address adverse human rights and environmental impacts. This directive transitions from voluntary frameworks established by organisations like the OECD and UN to legally enforceable obligations for companies.

Why was the CSDDD introduced?

The CSDDD was introduced to foster sustainable and responsible corporate behaviour by anchoring human rights and environmental considerations into companies' operations and governance. It addresses the shortcomings of voluntary due diligence practices, which often lacked legal consequences and were primarily driven by reputational risk.

What is the difference between the CSDDD and the Corporate Sustainability Reporting Directive (CSRD)?

The CSDDD is an "action" mandate that requires companies to actively identify and address human rights and environmental harms in their supply chains. In contrast, the CSRD is a "reporting" mandate that requires companies to disclose information on sustainability risks to the company and the company's sustainability impacts, focusing on what is known as "double materiality."

What is the current status of the CSDDD?

The CSDDD was first proposed by the European Commission in February 2022. After more than two years of negotiations and compromises, the directive received its final legislative approval on May 24, 2024. Member States now have two years to transpose the CSDDD into national law, with the implementation starting on a staggered basis from 2027, beginning with the largest in-scope companies.

Which companies are "in-scope" under the CSDDD?

The CSDDD applies to both EU and non-EU companies that meet certain turnover and employee thresholds. EU companies are in-scope if they have a net worldwide turnover of 450 million Euros and more than 1,000 employees. Non-EU companies are in-scope if they have an EU turnover of more than 450 million Euros, with no employee threshold. The directive also applies to certain regulated financial undertakings that meet these thresholds.

What are the exceptions or flexibility for groups of companies within the CSDDD?

The directive allows some flexibility for groups of companies. A parent company that is a purely holding company with no operational activities can designate an EU subsidiary to perform due diligence obligations on its behalf, subject to approval from the relevant authority. Additionally, a parent company may fulfil the due diligence obligations of its subsidiaries, although the subsidiaries remain subject to the supervision and civil liability of their respective Member States.

What are the staggered implementation timelines for the CSDDD?

The implementation of the CSDDD is staggered based on company size and financial thresholds:

- From 2027: Companies with over 5,000 employees and a net worldwide turnover of more than 1.5 billion Euros (EU companies) or a net EU turnover of more than 1.5 billion Euros (non-EU companies).

- From 2028: Companies with over 3,000 employees and a net worldwide turnover of more than 900 million Euros (EU companies) or a net EU turnover of more than 900 million Euros (non-EU companies).

- From 2029: Companies with over 1,000 employees and a net worldwide turnover of more than 450 million Euros (both EU and non-EU companies), as well as companies operating qualifying franchising or licensing models.

Kristy Duane

Kristy Duane, a corporate partner at CMS, advises listed companies and fund structured investors in the real assets sector. She has been advising since 2010 on ESG, particularly supply chain sustainability, which plays a crucial role in governance structures and investment decisions. Kristy has experience in helping companies plan for and integrate new regulatory frameworks, such as ESG regulations, into their businesses.

There are no available Videos from "Kristy Duane"